This one pager was written as Spartan Delta’s Duvernay wells started coming in stronger than expected. The original goal for me was to sanity check the upside, but once I dug into the numbers it became clear the market was still treating the Duvernay as optional when it was already showing repeatable economics.

The work focused on how Spartan’s Deep Basin cash flow base supports Duvernay growth without forcing the company to lever up. Higher condensate yields and better capital efficiency changed the profile of the asset. What used to look like longer dated upside was starting to show up in near term production, cash flow, and returns.

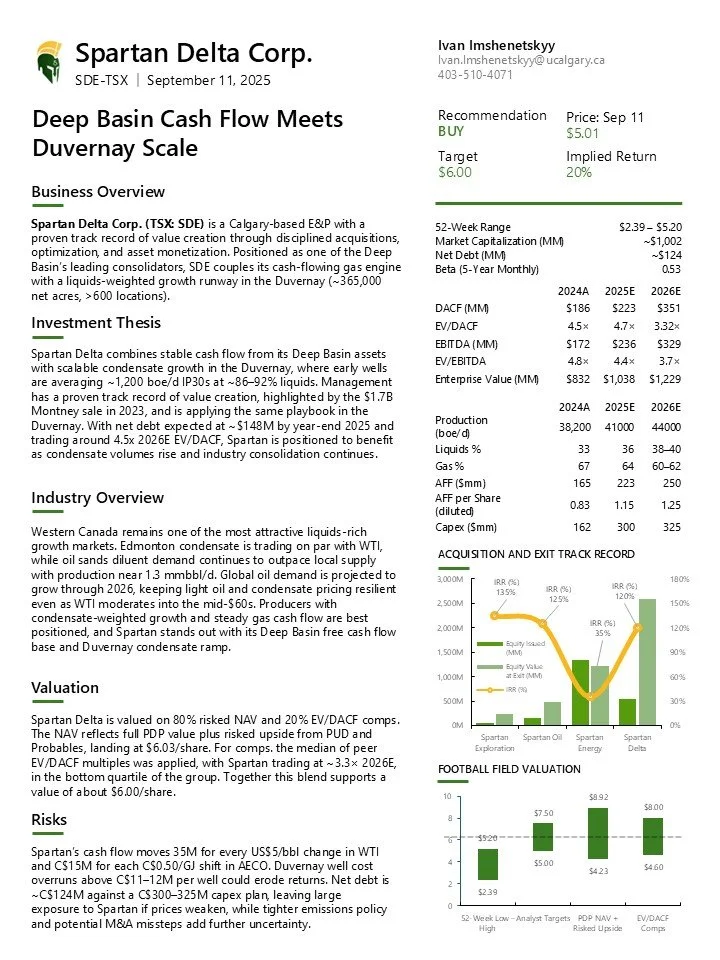

I updated production and capex assumptions and rebuilt the valuation using a mix of risked NAV and EV to DACF comps. As more locations moved from probable toward developed, value was pulled forward, which supported a $6.00 price target.

At this point, Spartan looked less like a single asset story and more like a liquids weighted consolidator with improving free cash flow and a clear path to higher returns as Duvernay development continued to scale.