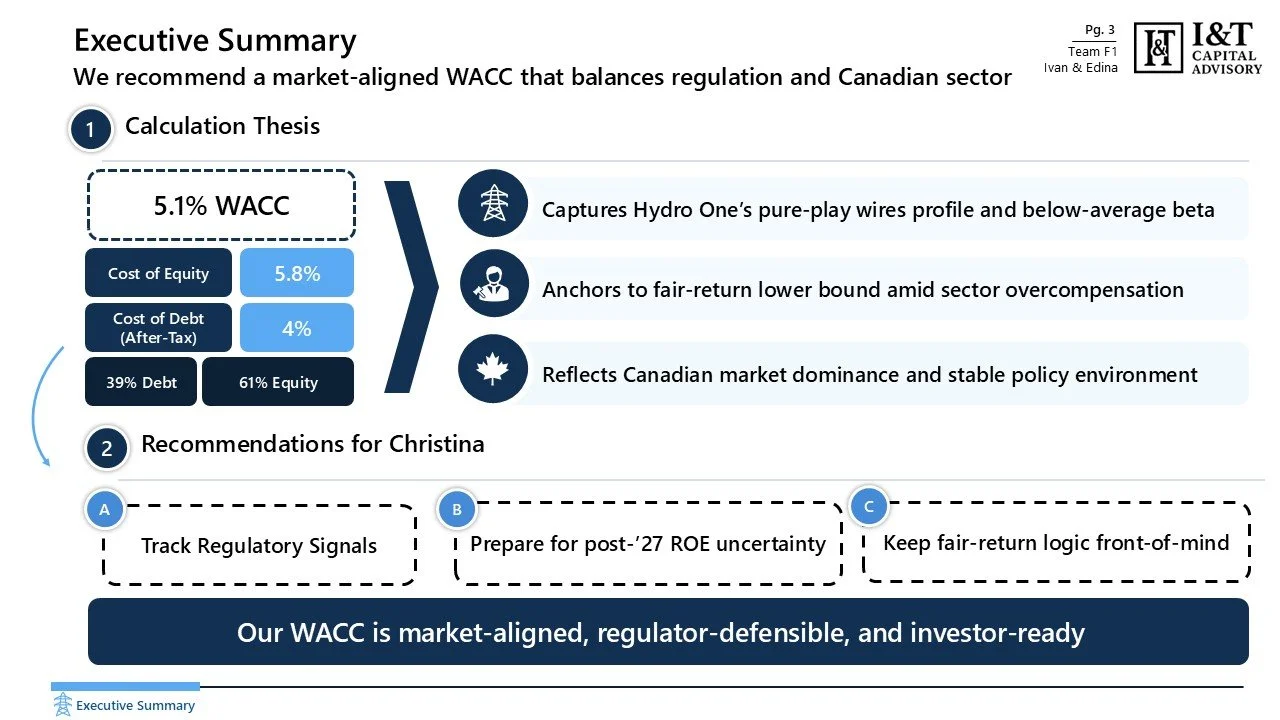

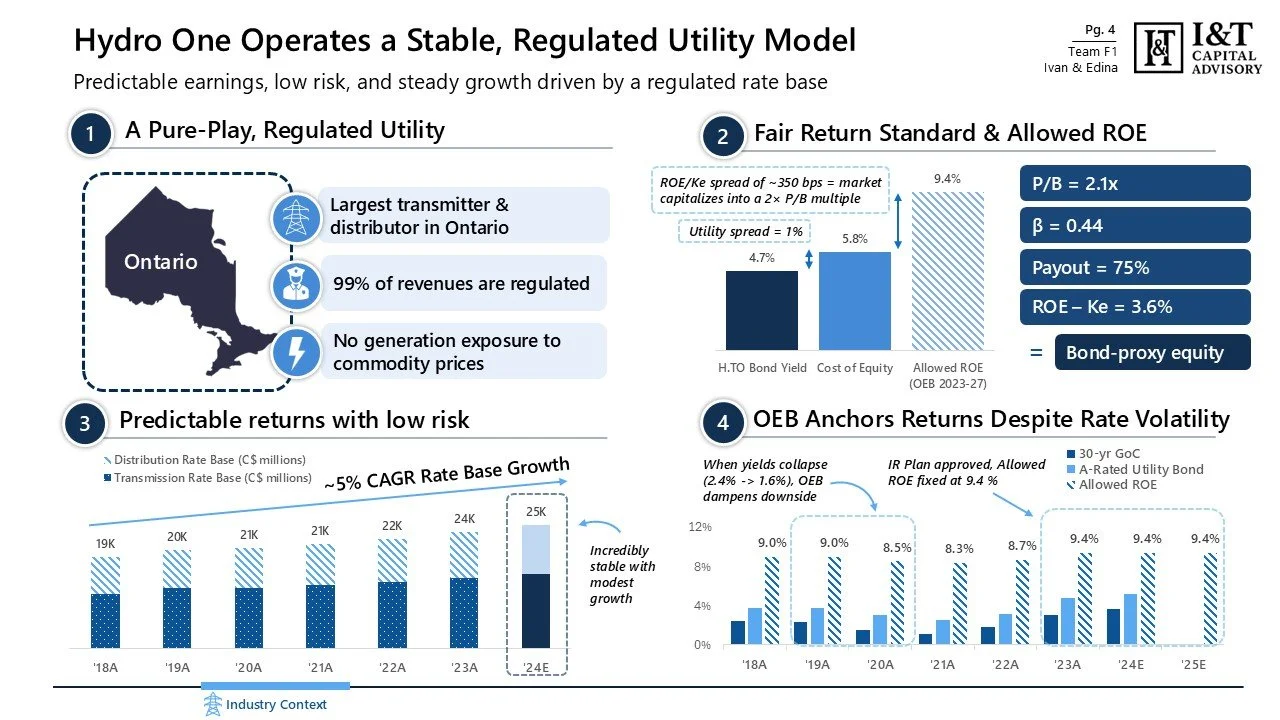

In the preliminary round, Edina and I were asked to advise an institutional investor on what looks like a straightforward question, What is Hydro One’s fair market cost of capital? In practice, utilities are a very different asset class. Returns are regulated, leverage is policy driven, and the allowed ROE set by the Ontario Energy Board matters more than most market inputs. We had two weeks, not much sleep, and no room to hand-wave assumptions.

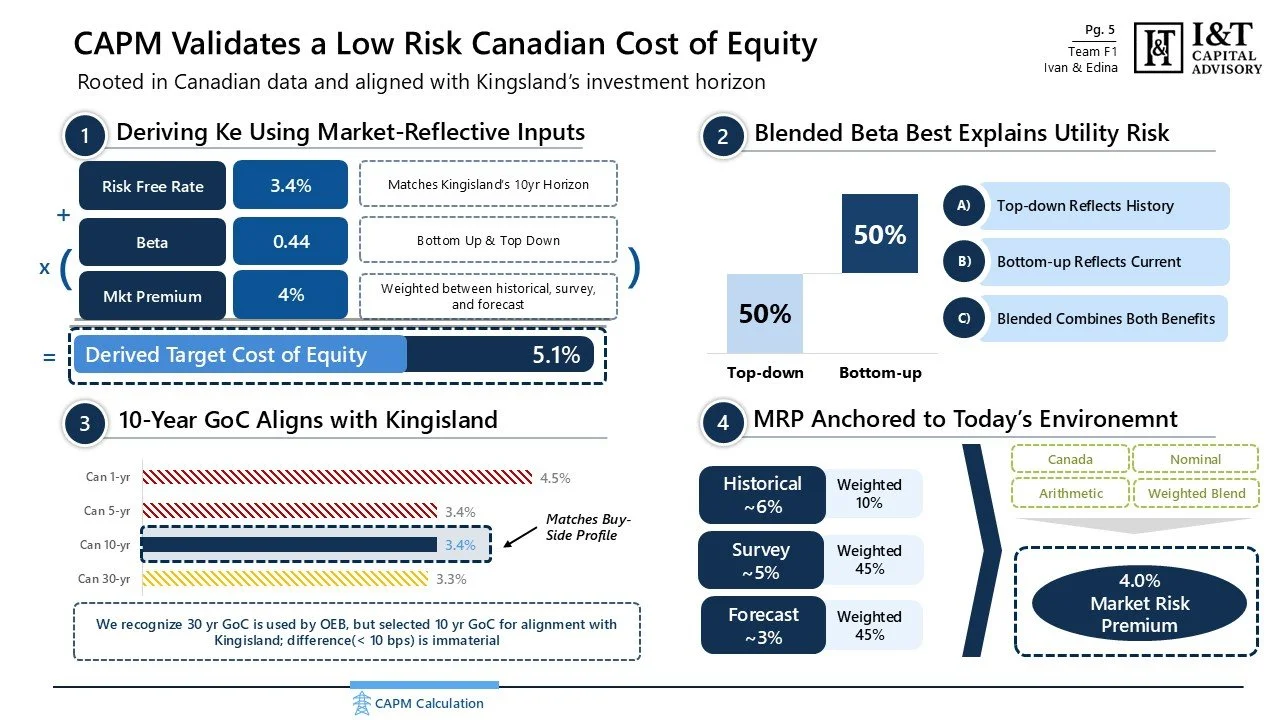

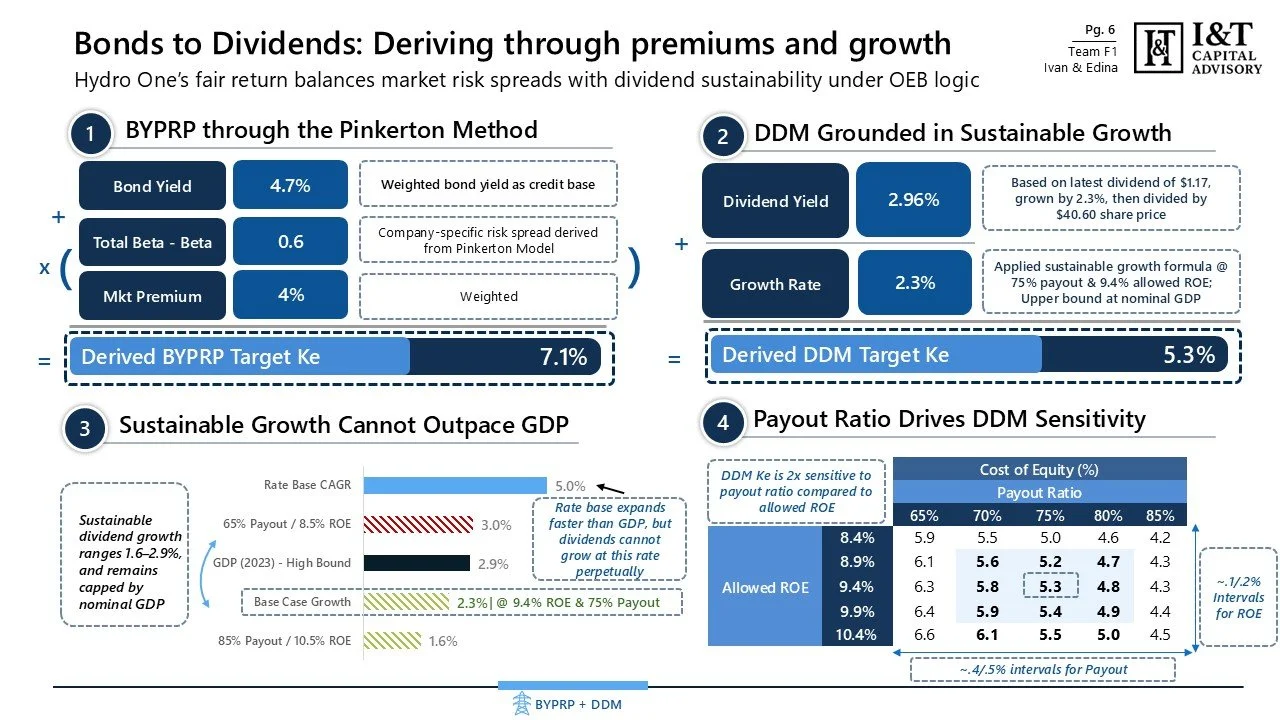

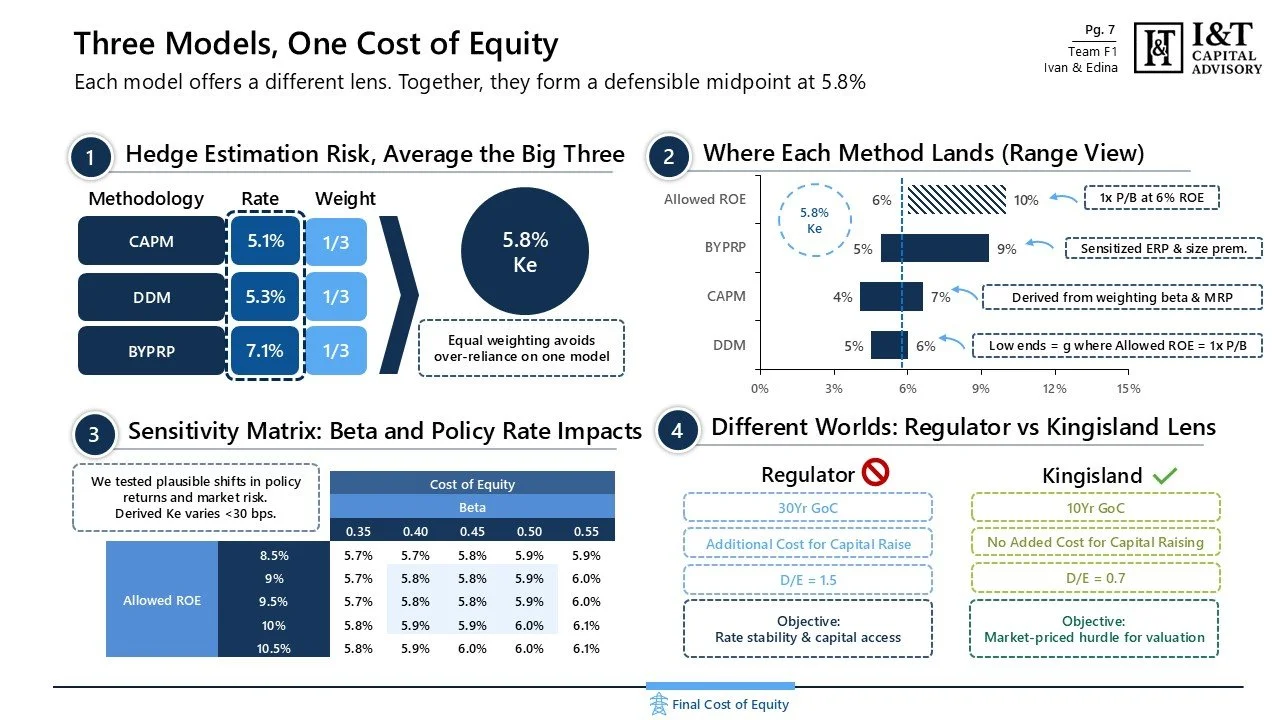

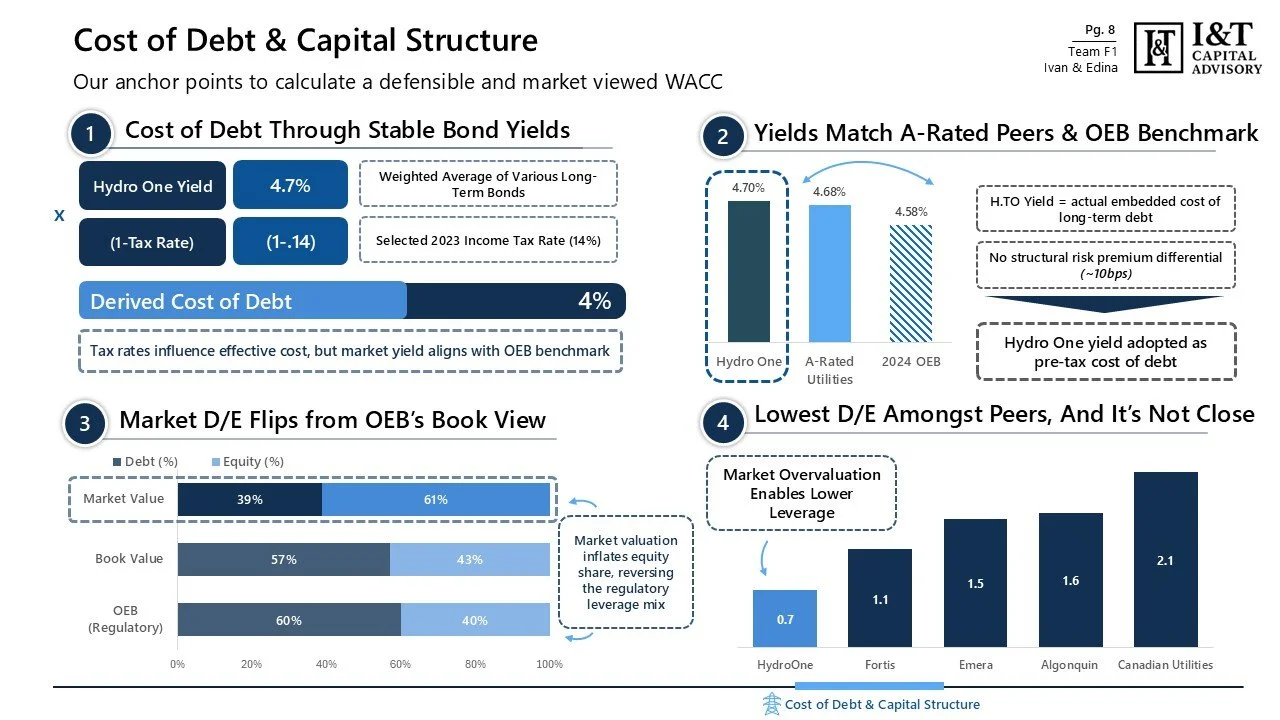

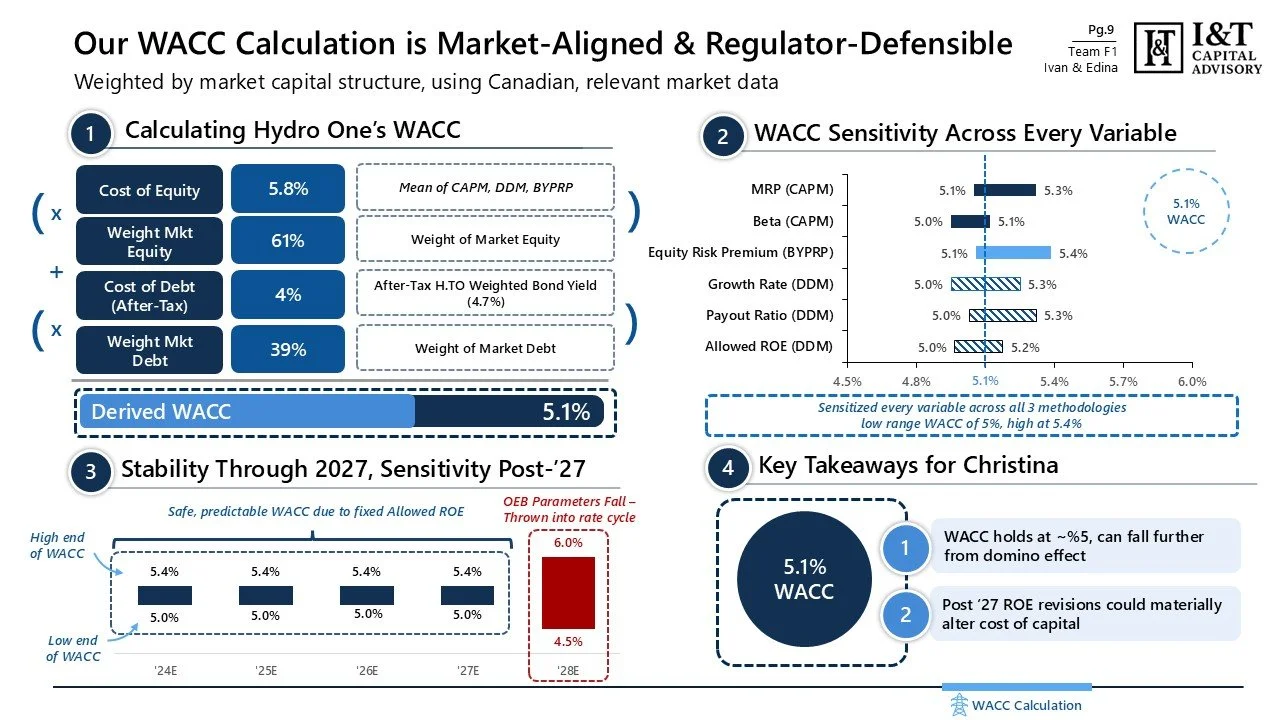

We built a regulator-defensible WACC using CAPM, dividend discount modeling, and the bond yield plus risk premium method, all anchored in Canadian data and OEB precedent. What mattered most was not the headline number, but how sensitive the result was to regulatory mechanics. In a regulated utility, payout ratios and allowed ROE drive equity returns far more than beta or growth assumptions.

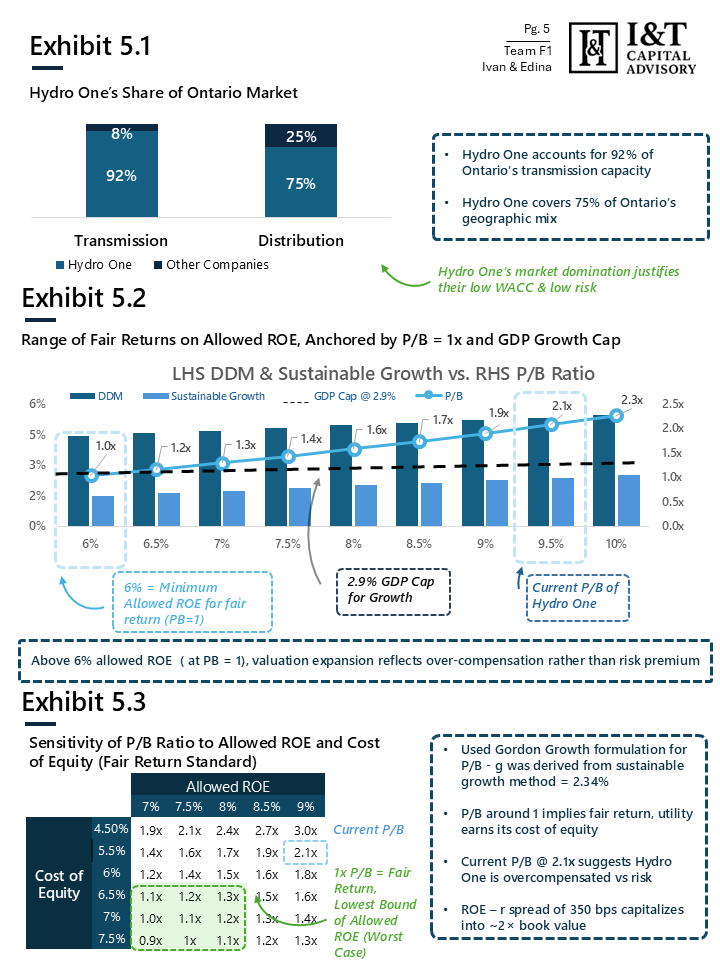

Through our analysis, we realized how overcompensated the utilities sector appears. The spread between allowed ROE and market-required returns helps explain Hydro One’s high P/B multiple and unusually low leverage. That dynamic framed how we thought about valuation today versus policy risk after the current ROE framework resets in 2027.

The final deck was built to be usable, not theoretical. It balances buy-side rigor with regulatory realism and is designed to support valuation work, portfolio decisions, and future rate proceedings. The full analysis and sensitivities are laid out in the deck itself.