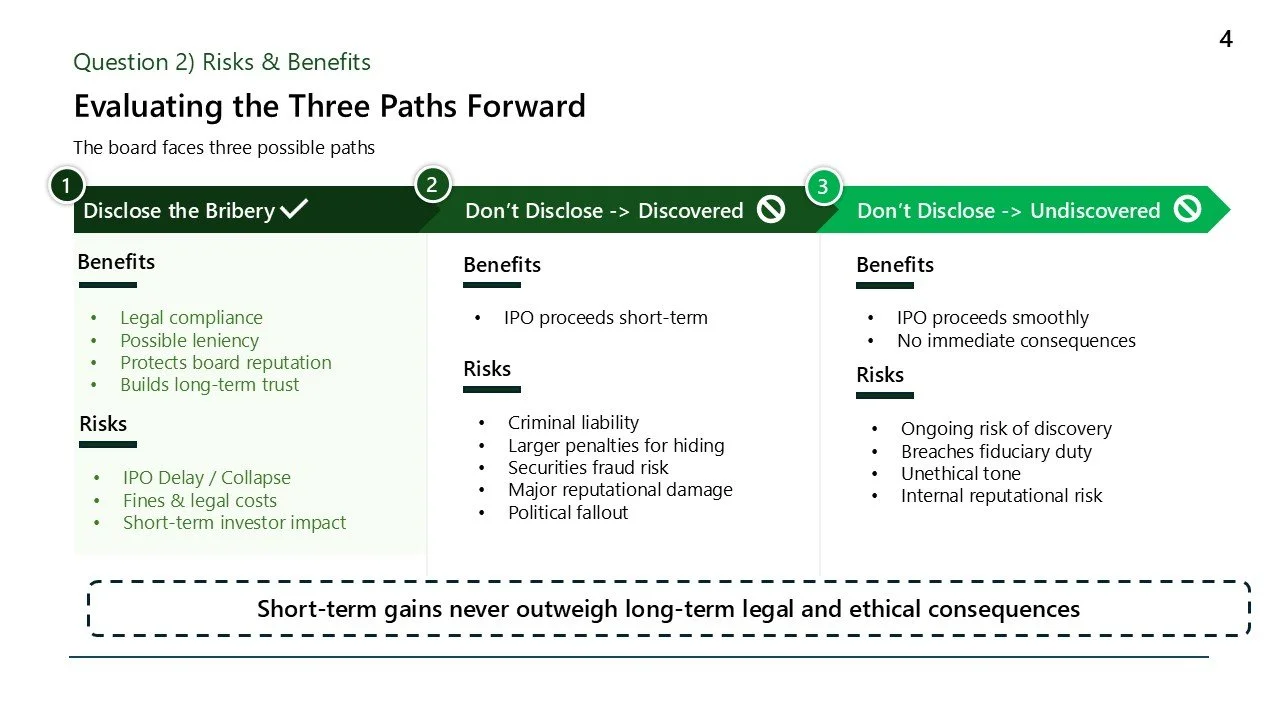

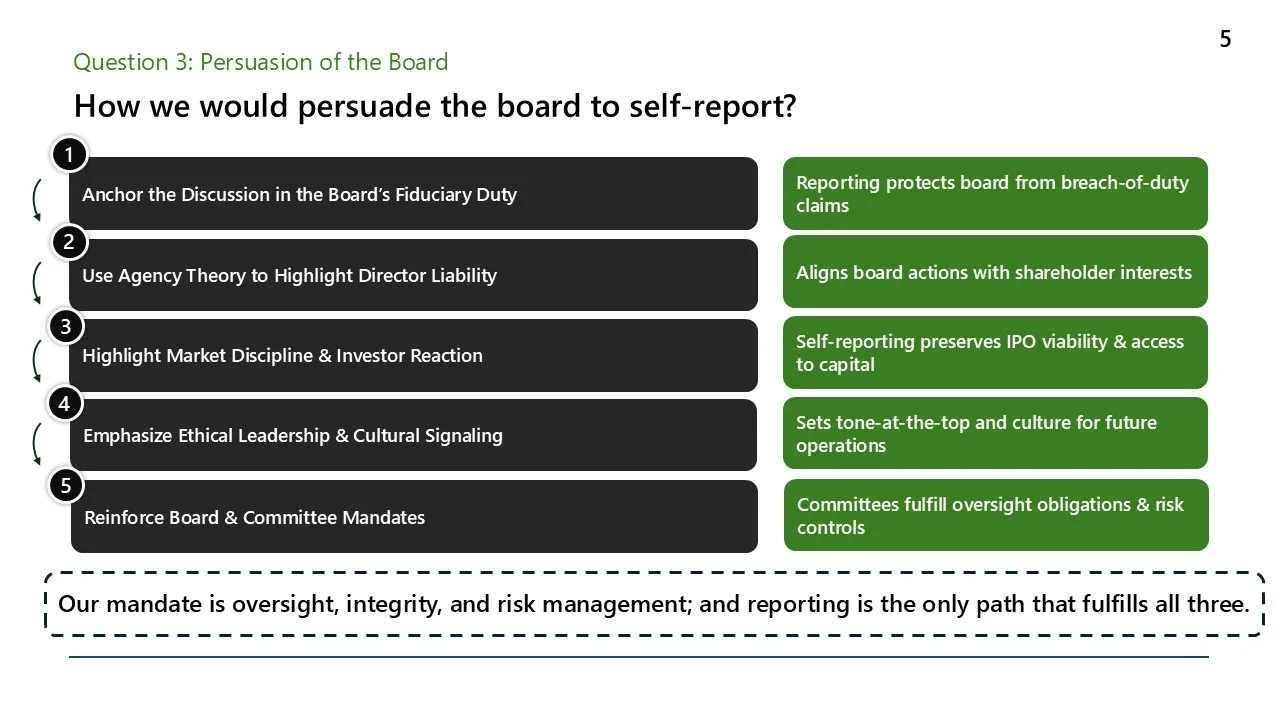

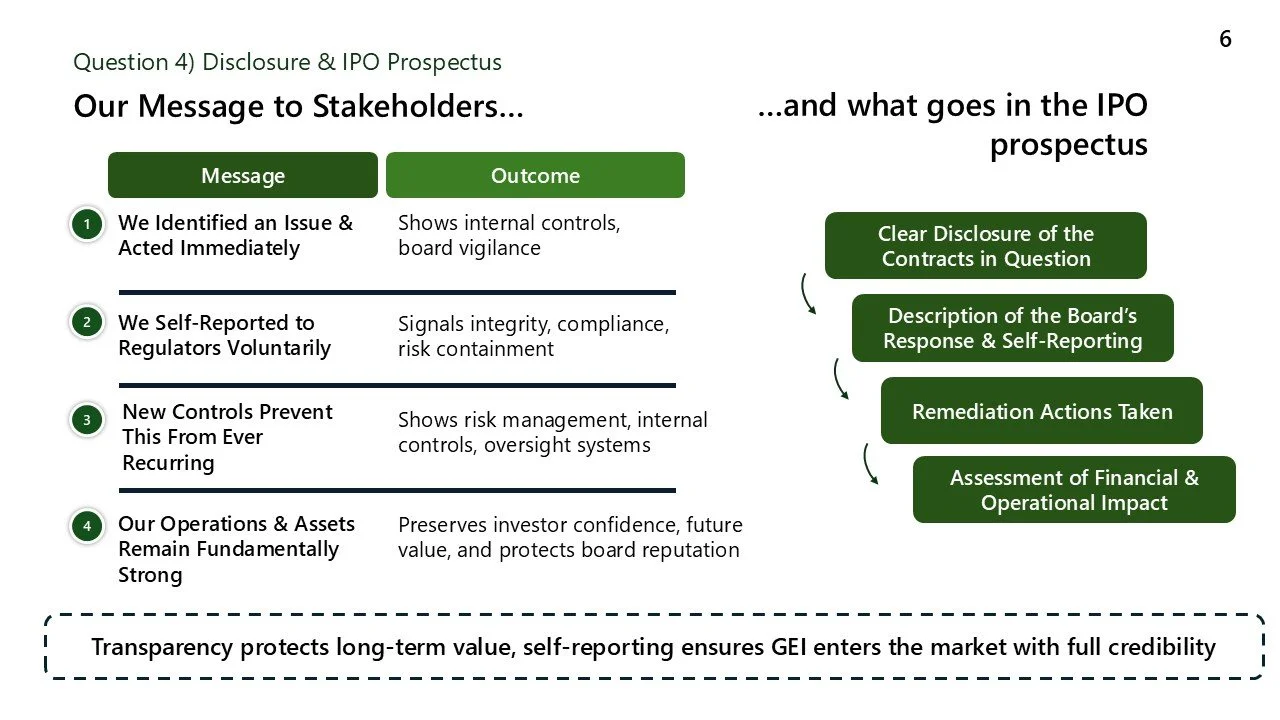

With an IPO approaching, Griffiths Energy faced a decision that could not be undone. A single contract raised the risk of undisclosed foreign bribery, placing the board under intense pressure to protect valuation, timing, and reputation. As disclosure deadlines closed in, the analysis followed the escalating tradeoffs between legal exposure, fiduciary duty, investor trust, and ethical leadership. The case demonstrated that silence offered short term comfort but long term destruction, while voluntary self reporting carried immediate cost but preserved credibility. The final recommendation positioned transparency not as damage control, but as a governance signal, concluding that self reporting was the only path consistent with board oversight, capital market access, and long term shareholder value.